Financial Accounting

Financial accounting is a specific branch of accounting involving a process of recording and reporting the myriad of transactions resulting from operations

Tel (305) 431-2601

Financial accounting (or financial accountancy) in the field of accounting concerned with the summary, analysis, and reporting of financial transactions related to a business.[1] This involves the preparation of financial statements available for public use. Stockholders, suppliers, banks, employees, government agencies, business owners, and other stakeholders are examples of people interested in receiving such information for decision-making purposes.

Financial accountancy is governed by both local and international accounting standards. Generally Accepted Accounting Principles (GAAP) is the standard framework of guidelines for financial accounting used in any given jurisdiction. It includes the standards, conventions, and rules that accountants follow in recording and summarizing and in the preparation of financial statements.

On the other hand, International Financial Reporting Standards (IFRS) is a set of passion able accounting standards stating how particular types of transactions and other events should be reported in financial statements. IFRS are issued by the International Accounting Standards Board (IASB). With IFRS becoming more widespread on the international scene, consistency in financial reporting has become more prevalent between global organizations.

While financial accounting is used to prepare accounting information for people outside the organization or not involved in the day-to-day running of the company, managerial accounting provides accounting information to help managers make decisions to manage the business.

Financial accounting is the preparation of financial statements that can be consumed by the public and the relevant stakeholders. Financial information would be useful to users if such qualitative characteristics are present. When producing financial statements, the following must comply: Fundamental Qualitative Characteristics:

Relevance: Relevance is the capacity of financial information to influence the decision of its users. The ingredients of relevance are the predictive value and confirmatory value. Materiality is a sub-quality of relevance. Information is considered material if its omission or misstatement could influence the economic decisions of users taken on the basis of the financial statements.

Faithful Representation: Faithful representation means that the actual effects of the transactions shall be properly accounted for and reported in the financial statements. The words and numbers must match what really happened in the transaction. The ingredients of faithful representation are completeness, neutrality, and free from error.

Enhancing Qualitative Characteristics:

Verifiability: Verifiability implies a consensus between the different knowledgeable and independent users of financial information. Such information must be supported by sufficient evidence to follow the principle of objectivity.

Comparability: Comparability is the uniform application of accounting methods across entities in the same industry. The principle of consistency is under comparability. Consistency is the uniform application of accounting across points in time within an entity.

Understandability: Understandability means that accounting reports should be expressed as clearly as possible and should be understood by those to whom the information is relevant.

Timeliness: Timeliness implies that financial information must be presented to the users before a decision is to be made.

Financial accounting is a specific branch of accounting involving a process of recording and reporting the myriad of transactions resulting from operations

Healthcare Accounting Services has always been the engine keeping the healthcare sector on the right track

Qualified Medicare Beneficiaries Prohibition on Balance Billing Providers and suppliers who submit claims to Medicare for services and supplies

What are Miami Accountants planning for the future? Gustavo A Viera, Miami Accountants talked with over 250 Accountants at Miami accounting show

Observers See Dangers in Burgeoning Consulting Practices at Major Accounting Firms

Accounting Services in Miami Professional and Affordable Services, Financial Reporting, Tax Preparation, IRS Representation, AHCA Consulting

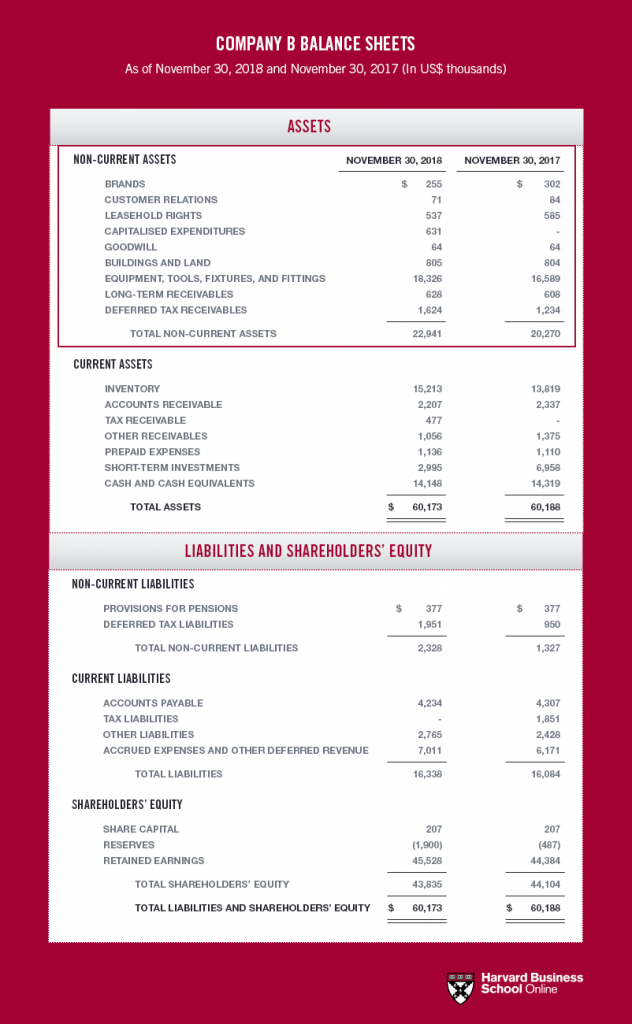

How to read a balance sheet In financial accounting, a balance sheet is a summary compiled by the Accountant of the financial balances of an organization

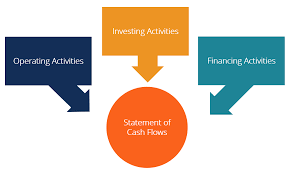

The Cash Flow Statement Shows Sources of Cash and cash equivalents and breaks the analysis down to operating, investing, and financing activities

Small Business Accountancy Steps to Tackling it Like an Accountant and why is it so important that accountants keep you informed of best practices

The Financial Accounting Standards Board has issued two proposed accounting standards updates meant to Income Tax Accounting