Small Business Accounting Best Practices: Cash Management

Small Business Accounting Best Practices: Understanding cash flow keeps the doors of your Business Accounting Firm open if you want to build on CPA Firm

Tel (305) 431-2601

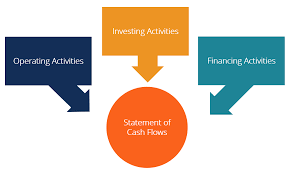

Cash Flow Statement In financial accounting, a cash flow statement, also known as statement of cash flows is a financial statement that shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing, and financing activities. Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. As an analytical tool Cash Flow Statement, the statement of cash flows is useful in determining the short-term viability of a company, particularly its ability to pay bills. International Accounting Standard 7 (IAS 7) is the International Accounting Standard that deals with cash flow statements.

Cash Flow Statement and the cash flow statement was previously known as the flow of funds statement. The cash flow statement reflects a firm’s liquidity.

The statement of financial position is a snapshot of a firm’s financial resources and obligations at a single point in time, and the income statement summarizes a firm’s financial transactions over an interval of time. These two financial statements reflect the accrual basis accounting used by firms to match revenues with the expenses associated with generating those revenues. Cash Flow Statement and cash flow statement includes only inflows and outflows of cash and cash equivalents; it excludes transactions that do not directly affect cash receipts and payments. These non-cash transactions include depreciation or write-offs on bad debts or credit losses to name a few. The cash flow statement is a cash basis report on three types of financial activities: operating activities, investing activities, and financing activities. Non-cash activities are usually reported in footnotes.

Small Business Accounting Best Practices: Understanding cash flow keeps the doors of your Business Accounting Firm open if you want to build on CPA Firm

Financial accounting is a specific branch of accounting involving a process of recording and reporting the myriad of transactions resulting from operations

The Cash Flow Statement Shows Sources of Cash and cash equivalents and breaks the analysis down to operating, investing, and financing activities

Cash Flow More Important is the Income Statement or Balance Sheet, Profit indicates business success, cash flow measures day-to-day basis staying power